Author: Scotty E. Chabert, Jr.

I guess you thought your insurance company was protecting you, right?

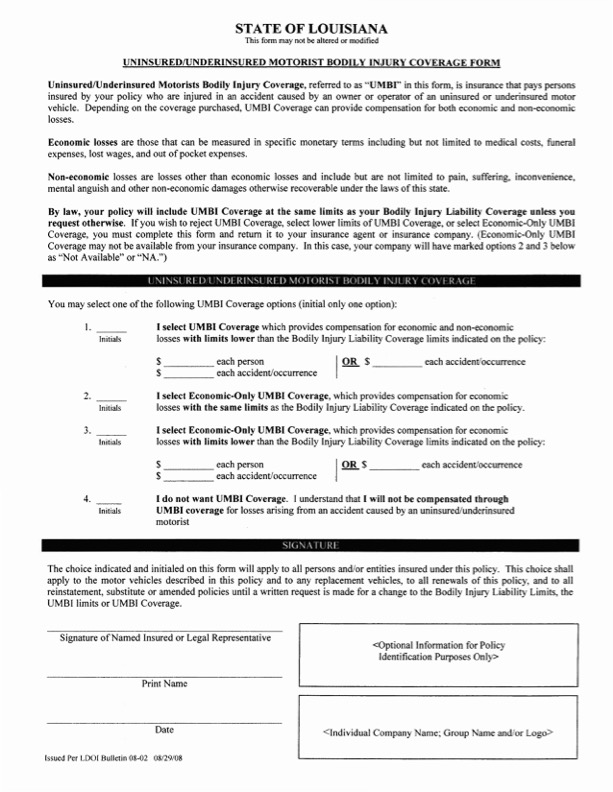

You get a letter in the mail, or maybe an automated email, while you’re renewing your policy. It looks official. It’s titled “Uninsured/Underinsured Motorist Bodily Injury Coverage Form.” It has a bunch of boxes, some legal jargon, and a line for your signature.

Naturally, you want to be a responsible driver. You want to make sure your paperwork is in order. You might even be tempted to fill it out online just to get it off your “to-do” list.

Stop. Put the pen down. Close the browser tab. Toss the form in the TRASH!

The Form is a Trick

Let’s be honest: If you’re like me and you spent three years in law school studying the complexities of insurance litigation, you might be able to figure this form out.

Just kidding. I think it’s a mess, too.

The form is designed to be confusing. It doesn’t clearly state the most important rule in Louisiana insurance law: You already have UM coverage. By law, if you have a liability policy, you automatically have Uninsured Motorist coverage that matches your policy limits. The insurance company isn’t sending you this form to give you something; they are sending it to see if they can trick you into waiving, lowering, or restricting coverage.

Why the “Trash Can” is Your Best Legal Defense

When you see this form, do not be fooled. Do not be confused. And most importantly: DO NOT SIGN IT.

If you want to keep your UM coverage (the coverage that protects you when someone else is irresponsible), the easiest thing in the world to do is… NOTHING!

How do you elect to have it? Just throw the form in the trash. By not signing and not returning that form, you are choosing to keep the full protection you are entitled to “by law” (that’s the insurance company’s own words)!

The 12% Reality Check

Why is this so important? Because nearly 12% of all Louisiana drivers are uninsured. That is 1 in 8 cars on the road next to you. And even more drivers are “Underinsured,” meaning they carry the bare-minimum 15/30 policy that barely covers a trip to the ER, much less a serious wreck.

Uninsured/Underinsured Motorist coverage is the cheapest insurance you can buy. It is the only part of your policy that is specifically designed to take care of you, not the other guy.

“But I Have Health Insurance…”

I hear this all the time. “Scotty, why do I need to pay for UM if I have good health insurance?”

Here is the truth: Health insurance pays the hospital. It does NOT pay your mortgage when you’re out of work for six months. It does NOT compensate you for your physical pain, your suffering, or the fact that you can’t pick up your kids because of a back injury.

UM coverage bridges that gap. It covers:

- Lost Wages: For the time you can’t work.

- Pain & Suffering: For the actual human cost of the accident.

- Special Damages: Things your medical insurance simply won’t touch.

The Saunders & Chabert Bottom Line

Don’t be fooled by a confusing piece of paper. You’ve worked hard for what you have; don’t let a “check the box” form take away your protection. If you’ve already signed one of these forms and you’re worried you’ve waived your rights, or if you’ve been hit by someone without insurance, contact our firm. We know exactly how to handle the “tricks” of the insurance trade!